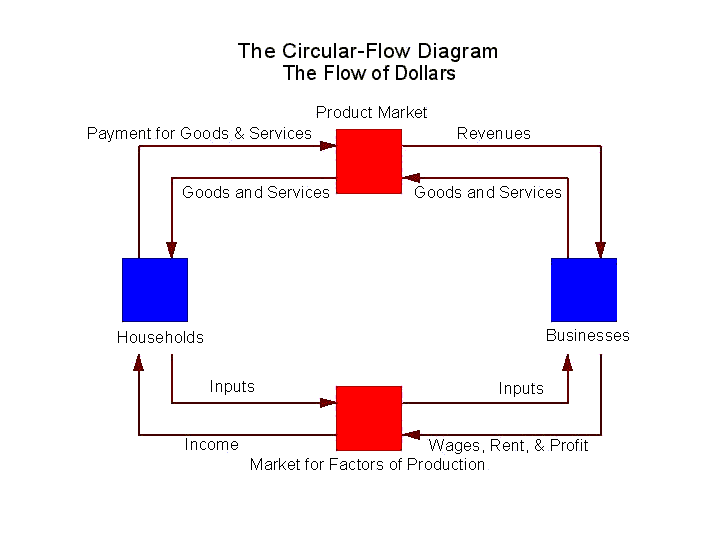

The circular-flow diagram is a simple model used by economists to explain how households and business are connected through markets. It assumes that households who own all resources and businesses produce all goods and services.

Households interact with businesses through two markets: the market for factors of production and the market for goods and services. The arrows that circle the diagram illustrate a physical flow and a financial flow. The inner arrows represent the physical flow. Resources or inputs are taken to the market for factors of production. Use rights to these factors are acquired by businesses that use them to make goods and transport them to the market for goods and services where they are acquired by households. The outer arrows represent the financial flows which move in the opposite direction. Households pay businesses for the goods and services they acquire in the market for goods and services. These revenues to the firm are used to pay their expenses in the market for goods and services. These expenses are the wages, rents, interest, and profit earned by households. Wealth is created through specialization. Markets allow households and businesses to specialize (Principle 8: A country’s standard of living depends on its ability to produce goods and services.). And (Principle 7) “governments can sometimes improve market outcomes” with good law.

Rajan and Zingales explain in “Saving Capitalism for the Capitalist” how households benefit from businesses ability to take ownership of collateral pledged to cover a loan.

Study after study has shown that the easier it is for a financier to seize collateral, the more lending takes place. The ease with which a creditor can collect on pledged collateral differs amoung countries. In England, or instance, it takes a lender on average a year and a sum of approximately 4.75 percent of the cost of the house to repossess a house from an insolvent borrower. Mortgage loans amount to 52 percent of gross domestic product (GDP) in England. In Italy, a country with roughly the same GDP per capita as England, it takes between three and five years at a cost of between 18 and 20 percent of the value of a house to foreclose on it. Mortgage loans amount to a far lower 5.5 percent of GDP.Likewise, businesses benefit from the bankruptcy code expands credit markets aiding both households and businesses as Rajan and Zingales offer this evidence.

The economic role of the bankruptcy law is not just to provide a mechanism for creditors to collect their money but also to offer a form of insurance to debtors, relieving them from some of their debt burden when it becomes overly oppressive. When a borrower owes so much that he has small hope of repaying it, he will have little incentive to exert effort to earn money, because any extra dollar earned, while requiring his blood and toil, will simply go to repay creditors. Both debtors and creditors may be better off in such situations if some of the debt is forgiven or renegotiated down in a bankruptcy proceeding. Debtors will have an incentive to work harder if they know there is some chance of repaying their debt and keeping their businesses, while creditors will get something back instead of nothing at all.Our laws governing collateral and bankruptcy may not be perfect, but they have improved credit opportunities for households and businesses. Good law creates wealth by creating opportunities for trade and specialization through markets.

{kind=link}

Glad to see the flow chart of this Home finance, homeowners have the ability to write-off the interest of the mortgage payments each month. In most cases, this saves homeowners thousands of dollars each year. Renting does not offer the tax advantages that owning a home enables.

ReplyDeleteLooking for Buy to let mortgage advice? Go at http://www.mortgageadvicebureau.com/buy-to-let-mortgage/